Fault Lines #3: Europe’s economic reckoning

An unfinished drama in three acts

“The difficulty is not so much to develop new ideas as to escape old ones.”

- John Maynard Keynes

As the EU emerges from the emergency phase of the pandemic, urgent questions loom about how it can overhaul its economic management and budget rules.

This extended post looks back at what has happened over the decade since the Eurozone crisis, and particularly the pandemic period, to understand whether it can steer a path through the interacting constraints it faces to construct a solution to its economic dilemmas.

Act One: Accounting for an eventful decade

Europe’s failed economic policy experiment came to a sudden halt in the Spring of 2020.

For the previous decade, as the preferred approach of fiscal tightening and monetary loosening played out, the EU lurched from one largely self-inflicted crisis to the next, as the deep flaws in the design of the Euro were exacerbated by repeated waves of policy responses that prolonged the Eurozone crisis.

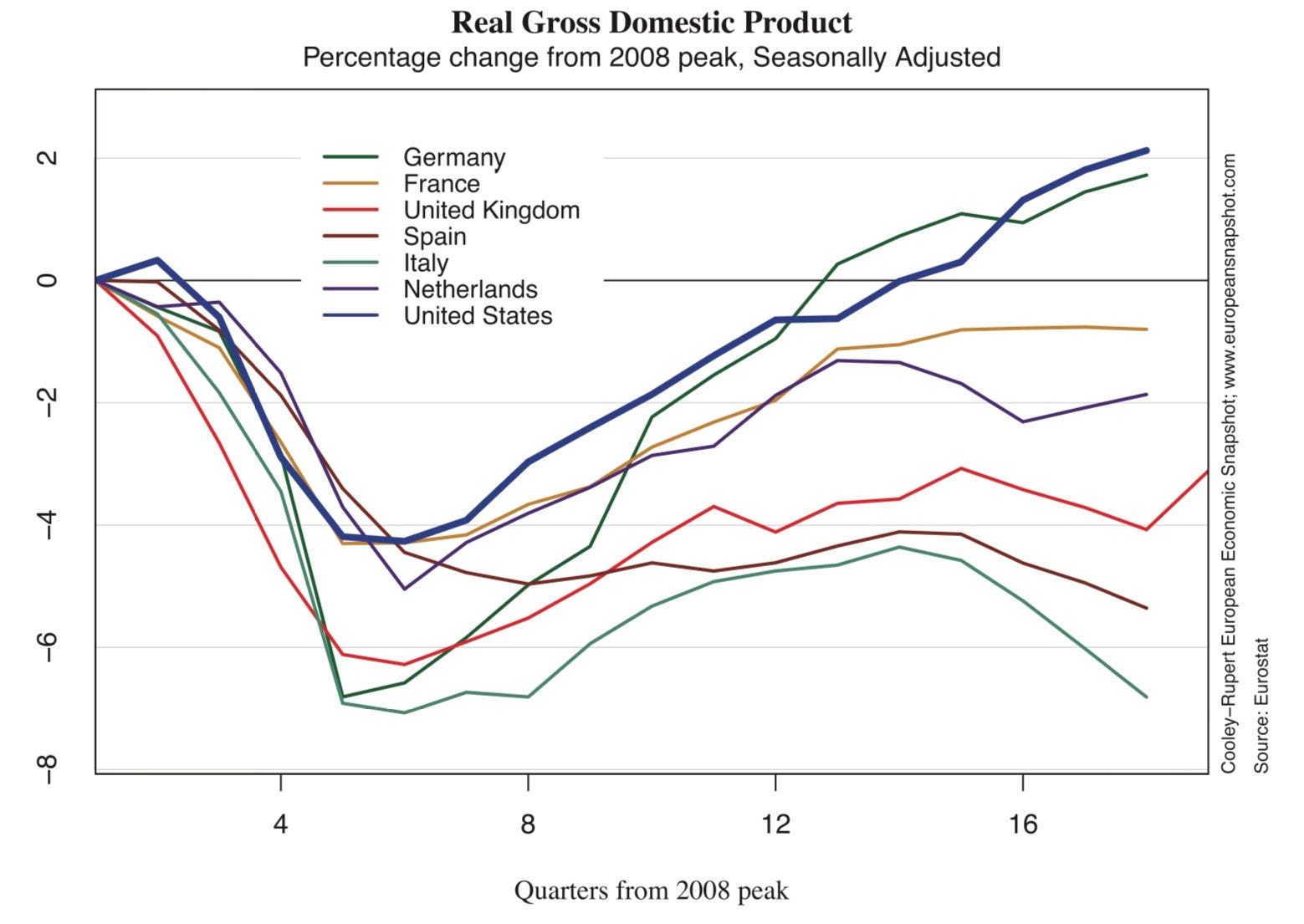

The extent of the EU’s failings during this time can be easily illustrated by comparing its economic recovery with the US. While America’s recovery from the Great Recession was sluggish by the standards of previous recoveries, it was day and night when compared to most European economies - with the notable exception of Germany:

US per capita GDP recovered to its pre-crisis peak in 2014, albeit that pre-pandemic the trend remained markedly below that prior to the Great Recession. While private investment contracted less in the Euro area than in the US during the 2008-09 crisis, investment in the Euro area continued to decline as a percentage of GDP between 2010-14, while the investment rate in the US began to recover in 2011.

The literature on the reasons for this divergence is vast - including some persuasive arguments that the narrative around comparative economic performance is not entirely justified. Differences in the treatment of personal debt, productivity and the comparative health of the EU and US banking systems all played an important part in this story and cannot be dismissed.

However, there is no doubt that the default fiscal policy of austerity - particularly when the constraints on monetary policy created by zero or effective lower bound on interest rates throughout much of the past decade is taken into account - played a significant role. Throughout the Eurozone crisis, fiscal policy was contractionary.

As former president of the ECB and now Italian Prime Minister, Mario Draghi, pointed out in his parting speech at the end of 2019, fiscal policy tightened at precisely the wrong time - and it impacted different countries in diverging and damaging ways:

The second factor was a change in the macroeconomic policy mix. While in the first phase of the crisis fiscal and monetary policy had eased in tandem – with fiscal policy loosening by a total of about 3% of potential GDP between 2008 and 2010 – thereafter the stance of monetary and fiscal policy decoupled. The euro area fiscal stance turned contractionary in response to the sovereign debt crisis, tightening by around 4 percentage points of potential GDP until 2013 – years the euro area was mostly in recession.

This stands in contrast to the United States, where fiscal policy eased more in the initial phase of the crisis, by about 6.5% of potential GDP in total over 2008-09, and then tightened by about 5.5% of potential GDP from 2011 to 2013 when the economic recovery was underway. The euro area was forced onto a different path by the need in some countries to re-establish fiscal credibility. But on aggregate the euro area did not have less fiscal space than the United States: public debt levels were similar in the two jurisdictions. The key difference was that fiscal stabilisation in the United States took place at the federal level, while the euro area lacked a central fiscal instrument to act counter-cyclically.

Draghi went on to bemoan what he called the institutional weaknesses of monetary union which could not be ignored any longer at the cost of seriously damaging its achievements to date and concluded with a démarche to Europe’s political leaders on the need to overcome their fiscal passivity:

Over the last 10 years, the burden of macroeconomic adjustment has fallen disproportionately on monetary policy. We have even seen instances where fiscal policy has been pro-cyclical and countered the monetary stimulus.

If the unbalanced macroeconomic policy-mix in the euro area in part explains the slide into disinflation, so a better policy mix can help bring it to a close. Monetary policy can always achieve its objective alone, but especially in Europe where public sectors are large, it can do so faster and with fewer side effects if fiscal policies are aligned with it.

Recreating fiscal space by raising potential output through reforms and public investment, and respecting the European fiscal framework will maintain investor confidence in countries with high public debt, low growth and low fiscal space. But as fiscal expansion in the other countries may have limited spillovers, national fiscal policies remain constrained. So work on a common fiscal stabilisation instrument of adequate size and design should proceed with broader scope and renewed determination.

Logic would suggest that the more integrated our economies become, the faster should be the completion of banking union and capital markets union, and the faster the transition from a rules-based system for fiscal policies to an institution-based fiscal capacity.

Draghi’s challenge to the failures of the policy during this period are now widely acknowledged not just by the persistent critics of the response to the Eurozone crisis, but by his fellow live players and key actors in the drama. Among these voices, none is more significant than Marco Buti, who was Director-General for Economic and Financial Affairs at the European Commission for the decade up to the end of 2019 and is currently Head of Cabinet for European Commissioner for the Economy, Paolo Gentiloni.

Buti’s recent book can be read as both companion to the crisis and cri de coeur from someone who understands the roots of the disaster that befell the EU during the Eurozone crisis.

At the heart of Buti’s reflection is a recognition of the divisions between member states and the European institutions that prevented the EU from pursuing the correct economic policy and replaced it with a series of sub-optimal instruments that were ill-suited to the reality of widely diverging creditor and debtor political economies. He writes:

During the financial crisis, the lack of trust amongst member states and between the latter and European institutions created suspicion in some countries about the use of any discretion in the implementation of the fiscal rules. This led to the attempt to codify all possible states of the world in complex algorithms so as to avoid discretionary decisions as much as possible. The over-engineering of the Stability and Growth Pact (SGP) is the quintessential example of this dérive.

However, as economic analysis and experience show, complete contracts do not exist. Moreover, the increasingly sophisticated algorithms, often based on unobservable variables, add to complexity which itself undermines the effectiveness and transparency of surveillance. If the rules of macroeconomic and fiscal surveillance are to be simplified, member states have to accept that the Commission applies them using the appropriate degree of economic judgement.

It is hard to do justice to the public service Buti has performed in providing us with an insight into the thinking of the Commission throughout the crisis. His suggestions for the reforms needed for the Eurozone to avoid a similar fate in the future - which I will return to later - are creative and politically feasible.

However, this should not insulate him from criticism, particularly when it comes to his argument that economic policy would be greatly improved if EU-level decisions were shielded as much as possible from domestic political economy considerations.

While domestic politics is the key constraint on the ability of the EU to move forward on many dimensions of integration - from fiscal policy to foreign and security policy and defence cooperation - it is the perception, and often the reality, of the insulation of policy from the domestic influence that has been at the heart of the disillusionment and disengagement of European citizens with the EU during the decade of crisis.

The same lack of trust that Buti decries often has its source in the perception of the European institutions among the political publics of member states. Whether this is Irish or Greek citizens who believe they were made to pay a disastrous price to save the EU’s financial system (something Buti acknowledges) or the millions of jobless youth in Southern Europe for whom the advent of the Euro was the start of a seemingly endless period of economic stagnation and lack of opportunities.

Indeed, Helen Thompson has gone so far as to argue that the labour migration away from those countries towards the UK, which became the “employer of last resort” for the Eurozone’s southern members in the years after 2011 indirectly contributed to the UK’s decision to leave the EU.

Implicit in Buti’s accounting of the EU’s response to the Eurozone crisis is a tension between the politics of technocratic rulemaking conducted away from the demands of democratic contestation and a politics of improvisation in response to uncertainty and events - a schema proposed by the Dutch political theorist Luuk Van Middelaar in his superb book Alarums and Excursions.

From Van Middelaar’s perspective, the decade of the Eurozone crisis saw a fundamental transformation in the character of the EU, moving away from the ‘quiet politics’ of technocratic rules to a more tumultuous form of power politics with the European Council comprising the national leaders at its centre. It is a transformation he welcomes, representing a historic hinge for the EU where its own destiny becomes a matter of ongoing political contestation and not trapped within a frozen legal order.

However, a problematic conundrum arises from Van Middelaar and Buti’s prognoses that goes to the heart of questions about the construction of a better economic policy and deeper fiscal integration in the aftermath of the pandemic:

If what is needed for European integration to advance is a form of intergovernmental power politics rooted in the democratic legitimacy of the European Council rather than the “community method” of supranational institutions like the Commission or the Court of Justice, how can this be achieved when any moves towards such integration are resisted by member states without agreed rules of the game to mediate their mistrust of each other, which can in turn only be managed by the supranational institutions?

These contradictions are central to the debate now underway on the best path forward for European economic management.

Next Week: Act Two - No Limits